Housing models with risky mortgages

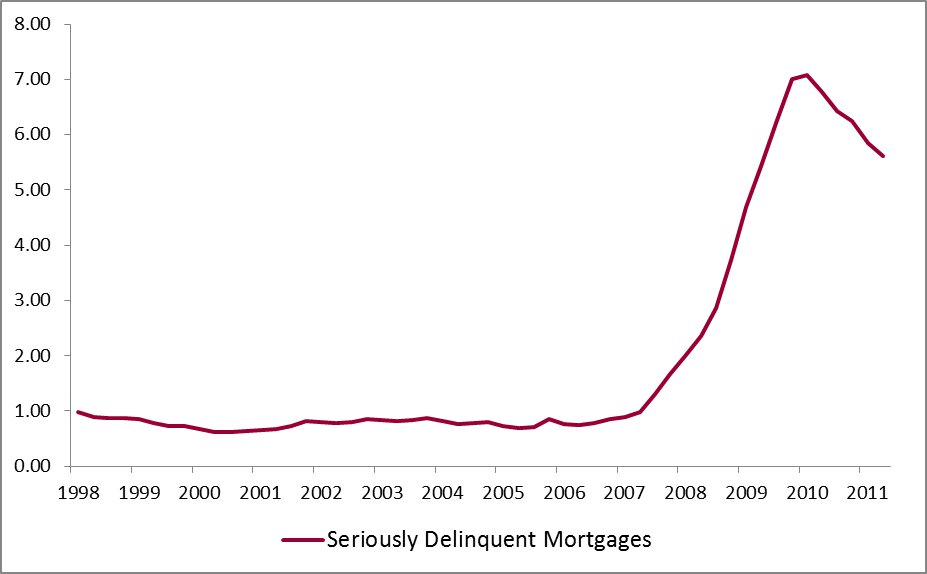

This project develops a model with housing and risky mortgages. The returns to housing are subject to aggregate and idiosyncratic risk. Mortgages are defaulted in equilibrium when housing returns are low. To capture recent events, we consider an increase in the riskiness of mortgages. An increase in mortgage risk raises default and generates a credit crunch and a recession.

Working Paper: Risky Mortgages in a DSGE model

Alternative mortgage contracts

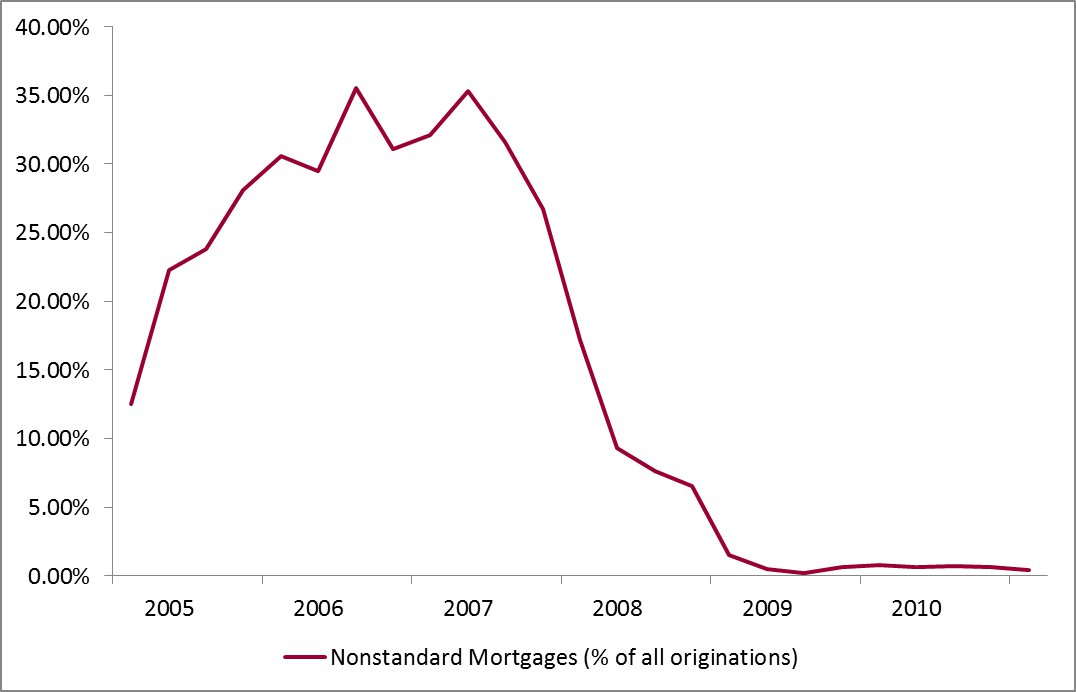

The recent financial crisis and the ensuing recession have their roots in the bursting of the housing bubble in the United States. Academic and Policy discussion have pointed to a number of likely contributions to the housing bubble, among which the appearance of exotic mortgage products (interest only, negative amortization and pay option Adjustable-Rate Mortgages). These nonstandard mortgage products share a feature: the reduction in the initial monthly payments relative to conventional Fixed-Rate Mortgage contracts. this project finds that low early or even negative amortization increases the default rate and intensifies the negative effects of a housing risk shock on aggregate consumption and output.

Working Paper: Mortgage Amortization and Amplification

Boom-bust cycles in the housing market

This project analyzes housing market boom-bust cycles driven by changes in households’ expectations. We explore the role of expectations on productivity and other shocks originating from the housing market, the credit market and the conduct of monetary policy. We